Carmignac's Note

![[Main Media] [Carmignac Note]](https://carmignac.imgix.net/uploads/article/0001/03/%5BMain-Media%5D-Carmignac%27s-Note_Market_Analysis.jpg?auto=format%2Ccompress "[Main Media] [Carmignac Note]")

Central banks perform a contagious, belated about-face

The outlook in this early part of 2022 is being marked by a resurgence of inflation, whose stubborn absence in recent years had fuelled worries about deflation and given central banks pretty much a free hand in setting monetary policy.

For over a decade, price inertia coupled with persistently sluggish economic growth allowed central banks to shore up their economies as and when needed, largely through cuts in short-term interest rates and quantitative easing policies that lowered the yields on long-dated paper. Central bankers – but also market participants, through their implied expectations and investment excesses – were able to “pick” what monetary policy they wanted to see implemented, with nothing to consider other than their own interests.

It was a period when bad news on the macro front, which came more frequently than good news, was actually a boon to financial markets because it meant central banks would turn on the liquidity taps, injecting more high-octane fuel into the system. But that was then. Now, and

as we predicted a few months ago, it’s inflation that’s “picking” the direction of monetary policy.

Central bankers have no choice but to bow to the whims of rising prices. That’s because central banks have a specific mandate to which they must adhere – and maintaining price stability is a central element of this mandate. Compromising on inflation would be a renegade act.

With inflation back at the helm of monetary policy, we can expect to see two main consequences. The first is a sharp increase in uncertainty about where interest rates are headed, as central bankers continually adjust their monetary policies in response to the vagaries of inflation. We’ll probably see a jump in the volatility of bond markets, and with them that of stock markets.

![[Divider] [Carmignac Note] Blue sky and building](https://carmignac.imgix.net/uploads/article/0001/11/be5cc29afb5283f73a810bcb5b36e50673c56e99.png?auto=format%2Ccompress "[Divider] [Carmignac Note] Blue sky and building")

Central bankers’ attempts to “telegraph” their monetary-policy decisions to investors so as to soften the immediate impact of those decisions will often fail. We’ve already seen caricatural examples of this with the US Federal Reserve’s shift in discourse once Chairman Powell realised in November (strangely late in the game) that inflation is here to stay. Ditto for the European Central Bank (ECB) even more recently, with the change in tone by President Christine Lagarde.

This about-face by the two central banks – which swung from denying inflation’s stickiness to announcing a possibly substantial number of rate hikes, potentially coupled with a brisk pace of quantitative tightening – is just a taste of the destabilising, unpredictable swings promised by inflation, and of the challenge policymakers will face in managing that inflation through a regular by-the-book process. Volatility is back!

Source: Bloomberg

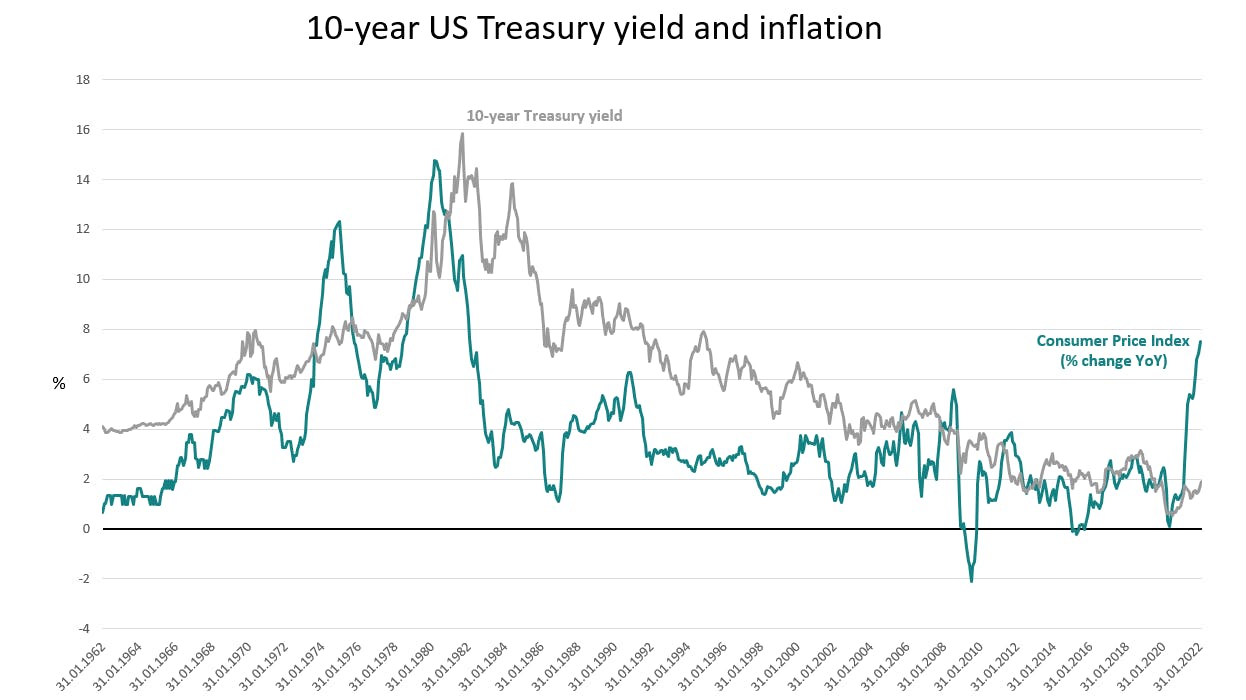

It is again inflation that’s ‘picking’ the direction of monetary policy

The second consequence of inflation’s comeback is that central banks, in order to comply with their mandate, will have to withdraw liquidity from the financial system – just when the economy is slowing. It looks like that’s where the US is headed today and possibly Europe in the near future.

The current trajectory of the US economy is a real dilemma for the Fed. GDP growth will likely slow from over 5% today on an annualised basis to a more modest 2% in the fourth quarter, while inflation will likely stay above 7% until March and then ease to a still-too-strong 3% by the end of the year. This confluence of factors calls for tighter monetary policy to make sure inflation stays close to the target of 2%.

Such tightening, however, will generate a considerable amount of anxiety, given that the market consensus believes neither that inflation will stay above the target for long nor that economic expansion will remain this strong (a view shaped by 40 years of disinflation and over 20 years of anaemic GDP growth). Some observers will accuse the Fed of a monetary-policy gaffe; others will point to the risk of a rebound in deflationary pressure.

This scepticism regarding the staying power of inflation could have a substantial effect that Mr Powell will want to rectify. His short-term rate hikes will likely be accompanied by an only moderate increase in long-term rates (resulting in a flatter yield curve), since investors still believe that the Fed’s moves will be enough to undercut expectations for inflation and GDP growth, and are therefore keeping long-term rates relatively low.

However, an only marginal rise in long-term rates would not be welcomed by the Fed, as it would view such an outcome as potentially watering down its monetary policy. The Fed needs to cool the US real-estate market, which is showing numerous signs of overheating. And because this market is sensitive to long-term interest rates, the Fed will want to see those rates climb significantly.

America’s housing market in particular has become increasingly speculative with an influx of investors seeking lucrative returns, to the detriment of first-time home buyers who are being sidelined by soaring house prices. All this leads us to believe that Mr Powell will pull the quantitative tightening lever as early as this year, because that would have a direct effect on long-term interest rates.

![[Divider] [Carmignac Note] Buildings](https://carmignac.imgix.net/uploads/article/0001/09/93e88f0c2250b1e9bd208f73682a149c7b77d746.png?auto=format%2Ccompress "[Divider] [Carmignac Note] Buildings")

Developments in the US will be decisive for the path taken by the ECB

Another factor that could explain Mr Powell’s about-face is that this business cycle appears to be unlike any other. The Fed will be tightening monetary policy at a time when economic agents are in a comfortable position financially, thanks to the large-scale fiscal and monetary stimulus programmes that governments rolled out to counter the effects of the pandemic and that could make consumers less vulnerable to monetary tightening.

Nevertheless, we shouldn’t summarily dismiss the consensus’ scepticism about the lasting nature of US inflation. The deflationary fears which shaped market movements over the past decade are still very much with us, notwithstanding the bout of inflation currently afflicting the global economy. Inflation of around 2.5% in two years’ time is a credible prospect, although such a forecast doesn’t account for some potentially inflationary structural changes such as higher energy prices, lower savings rates due to demographic trends, and planned repatriations of production plants.

In the near term, if the slowdown in economic output ends up impacting inflation more than expected, analysts could start toning down their forecasts for the scale of the monetary tightening to come, especially since the Fed will probably want to maintain some of the lag it has accumulated, insofar as possible. We can’t rule out a pleasant surprise on the monetary-policy front, but that’s not our core scenario.

Meanwhile, Ms Lagarde, who holds the eurozone’s monetary fate in her hands, has also undergone a radical change of course that could pave the way to monetary tightening already this year. We’re intrigued by what the “revelation” could be that prompted her new stance, given that the main factor driving eurozone inflation today – energy prices – is largely out of the ECB’s control.

Is she expecting a round of vindicative wage negotiations in Europe that could trigger a inflationary spiral like the one seen in the US for nearly a year? It’s a valid concern. Beware of sleeping dogs that have lain too long. But it’s worth first keeping an eye on developments in the US, as they will be decisive for the path taken by the ECB.

This new year is certainly shaping up to be volatile, eventful, and brimming with opportunity. It will be a year of challenges and surprises – suited much more to our active investment style than the spate of recent years when returns were nothing more than the frustrating result of a single, pedestrian decision: remaining passively invested.

Investment strategy

Source: Bloomberg, 04/02/2022

1Following a week in which the US Federal Reserve, the Bank of England, and the European Central Bank all adopted a more hawkish tone on inflation.

2Inflation was expected to peak last November, but is now predicted to top out in February or March at 5.5% year-over-year in the eurozone.

3Short-term yields, which are more sensitive to monetary-policy decisions, have risen to a greater extent than yields on longer-dated paper.

4They’re now above their 3-year moving average.

5The MOVE index has shot up to nearly 90 and surpassed its March 2020 highs.