Flash Note

The active edge: Constructing a diverse bond portfolio

The various episodes of stress on bond markets over the last twenty years have provided an opportunity for active management to shine. The change in the interest rate regime provides a good opportunity to reflect on the consequences and implications for fixed income investors.

After a more than a decade, the continuous fall in interest rates, synonymous with the rise in the valuation of assets and the neutralisation of credit risk by central banks came to an abrupt end. Active management of bond portfolios, including steering the exposure to different parts of the yield curve, allocating to different fixed income segments, managing modified duration, and implementing a rigorous analysis of issuers’ fundamentals are once again crucial tools for any investor.

The previous twenty years have been very favourable for bond markets. The fall in interest rates and unprecedented asset purchase programmes by central banks, saw the Bloomberg Euro Aggregate Bond index, which combines sovereign and corporate bonds, return over 70% between mid-2003 and mid-2023. This performance has at times been on a par with equity markets, but without the heightened volatility. In an environment like this, it’s little wonder the value of active management might sometimes have been questioned, even though many active strategies outperformed their indices.

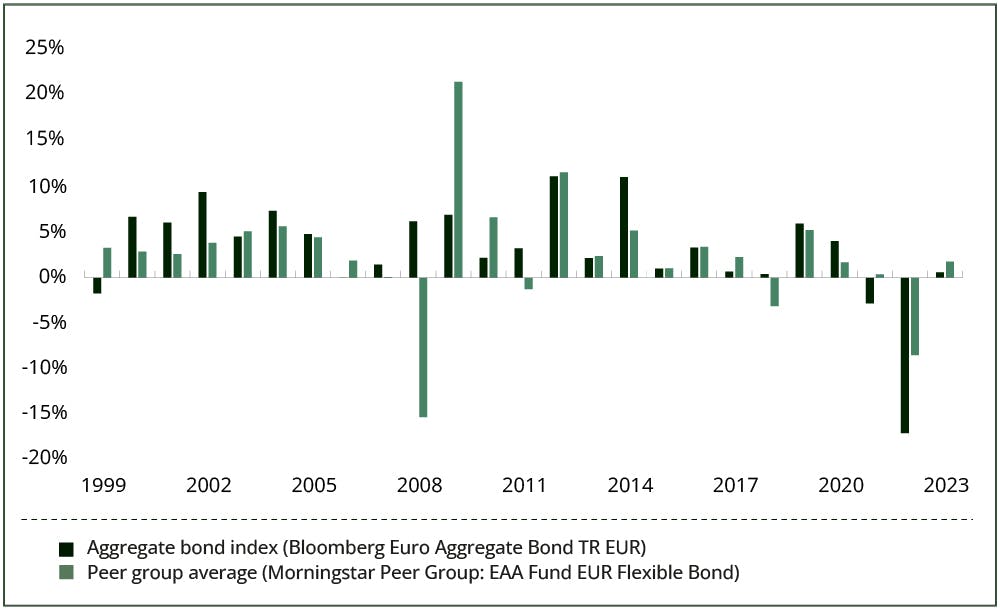

And lest we forget that active managers don’t simply participate during bullish phases. There were plenty of episodes of market stress during which the resilience of active management stood out. Indeed, the outperformance of active management over this period is best illustrated during three periods of volatility. Firstly, in the wake of the great financial crisis, during the European sovereign debt crisis1. Secondly, amid the ‘taper tantrum’ of 20132 and thirdly, more recently, the return of inflation and the reversal of central bank monetary policies in 20223.

Calendar year returns of the Euro Aggregate index and the Morningstar EUR denominated Flexible Bonds category

Less directional bond markets

The once unconditional stimulation of the economy by central banks has ended. Monetary authorities are determined to contain inflation, and will prioritise this over supporting growth. Central bankers will no longer play an outright reactionary role, meaning they will no longer offer the same support to bond markets and the economic cycle will kick back into action. For investors, this means static exposure, based on a simple index replication capturing various segments of the fixed income universe (sovereign debt, corporate bonds, investment grade or high yield, emerging debt) and different points of the yield curve, will no longer be enough to ensure a regular return, with proper risk management.

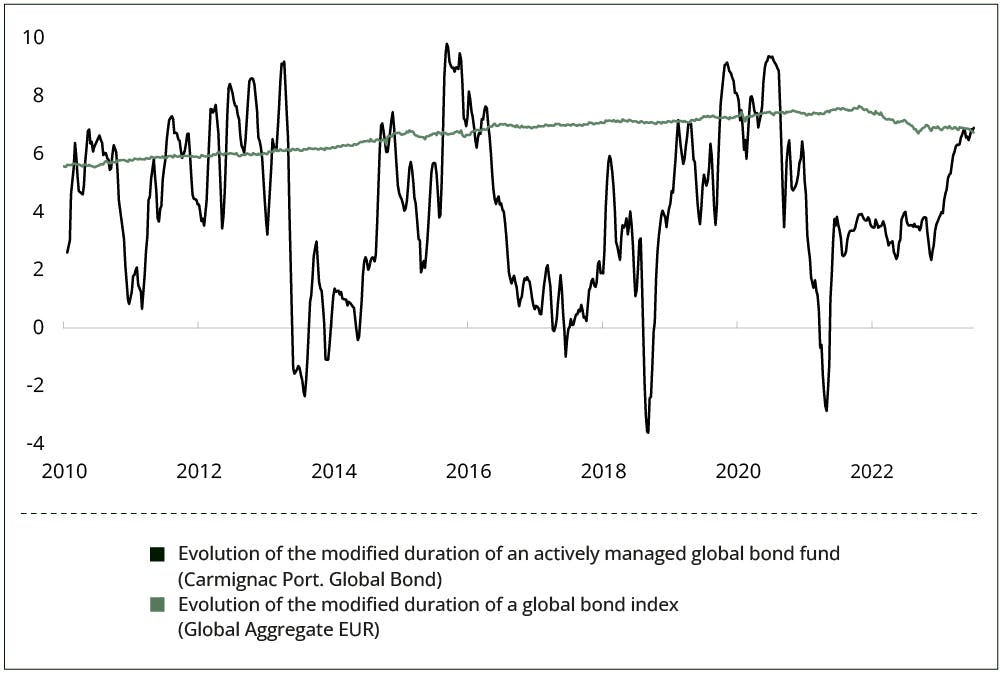

Today, bond managers need to be proactive, adjusting the maturity and the modified duration of their portfolios, as it once again becomes a strong driver of performance. A dynamic allocation, favouring certain segments of the bond market, the long or the short end of the yield curve, or even taking short positions on certain parts of the curve, is essential. This dynamic constitutes a major divergence from passive investing, where sensitivity to changes in interest rates cannot be adjusted, whether the environment is highly volatile or, on the contrary, directional. This is particularly important, as the steering of a portfolio’s modified duration is vital at economic tipping points. Today, on European bond markets, the modified duration is on average around 600 basis points (bps)4, by comparison, within the Carmignac fixed income management framework, a fund manager can vary the modified duration of their portfolio between for example, -350 bps (in October 2018) and +900 bps (in August 20205), depending on their choice to be more or less exposed to interest rate movements.

Evolution of the modified duration of an actively managed global bond fund and of a global bond index

Rising default rates

Credit risk – an assessment of an issuers’ financial health - is the second performance driver of fixed income markets. We have just come through a period of “free money”, when interest rates were so low that companies were easily financed, sometimes despite questionable fundamentals. Low default rates make credit risk analysis less effective. There was little need to distinguish issuers in good financial health from those in poor financial health; and so, there was little risk in maintaining some form of passive exposure to the latter. Dubbed the “financial repression”, the conditions offered by sovereign and corporate issuers to bond investors were poor remuneration for the risk taken.

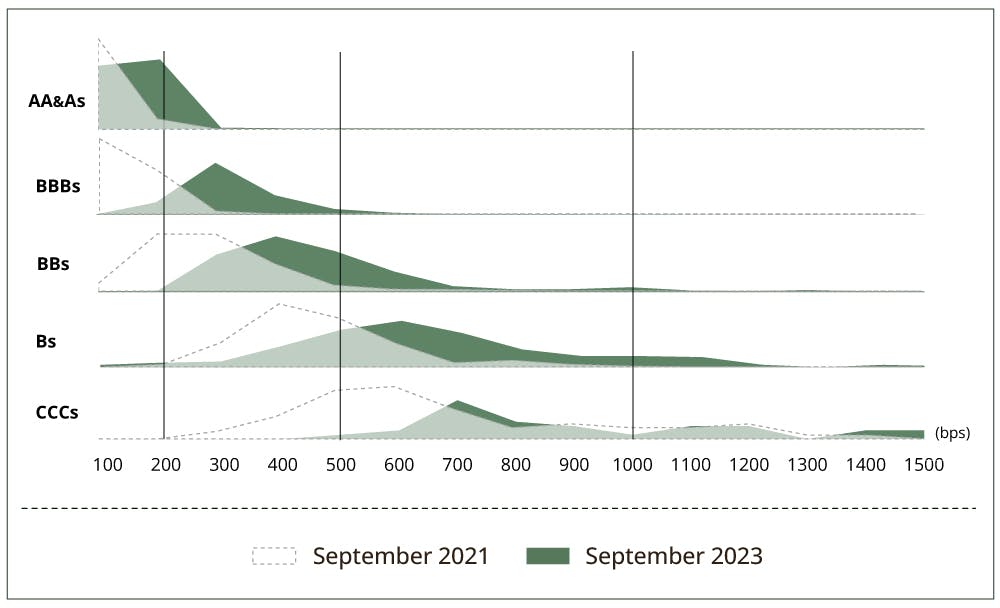

Convergence of risk premiums on credit markets : evolution of yields by credit rating bucket, in %

In March 2021, around 20% of the global stock of sovereign and corporate bonds6, more than €11,000 billion, were trading at negative rates. Now, for the worst performers, the horizon has darkened. Rising borrowing rates are putting pressure on the most heavily indebted issuers, who have also been weakened by the economic slowdown.

Default rates have started to rise again, and high-yield issuers must pay coupons of 7-8%, and sometimes even more than 10%, compared with 3-4% previously. The current default rate in Europe is 2.8%, broadly in line with historical averages but Moody’s expects it to rise to over 4% by May 2024. At the end of 2021, it was just 1.2%. Given this outlook, it would be risky not to try to separate the wheat from the chaff. A sound approach will consist in identifying issuers offering attractive yields for a controlled risk and ruling out more fragile issuers (from both a fundamental and/or a valuation perspective). Indeed, rigorous analysis and great selectivity are all the more essential as markets can be overly optimistic and securities of certain issuers trade at excessively high valuations, with particularly high spreads in the light of their potential future prospects. Dispersion of yields among issuers and issues is particularly wide: the average spread among BB-rated euro issuers was 400 bps (at 31/08/23) but within that rating bucket, some had a credit spread of less than 200 bps while others had a spread of close to 1,000 bps.

Distribution of credit spreads within EUR credit indices by credit rating bucket, in basis points

The chart illustrates the evolution of dispersion within credit indices. To illustrate dispersion, within each credit rating bucket we break down European corporate credit indices by level of credit spread today (dark areas are as of September 2023) and two years ago (transparent and dotted areas are as of September 2021). Two elements stand out. First, the distribution of credit spreads has shifted to the right: credit risk premiums have risen overall. And second, the distribution curves have flattened and widened: dispersion has increased, with wider spreads among issuers with a similar rating.

This increase in dispersion suggests that the link between perceived credit risk and its remuneration is more “blurred” than it was two years ago. This configuration is a source of opportunity for active portfolio managers capable of assessing fundamental risk.

The benefits of implementing a diversified approach to allocation within a broad universe

-

The recourse to passive investing implies the necessity to take a specific view on the bond market segments to which an investor seeks to gain exposure (investment grade credit, high yield credit, financial debt, developed markets, emerging markets, etc.). However, in reality, it can be difficult to formulate such a view, especially in an increasingly complex market environment. We therefore believe that the best strategy is to adopt an agnostic approach by maintaining the leeway to invest in several fixed income segments. This strategy has two advantages.

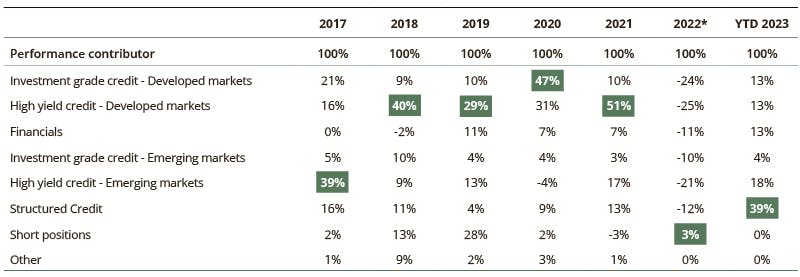

The first is that a diversified allocation enables investors to benefit from the complementary nature of the different fixed income segments. For example, in a market phase such as the one seen in 2022 and 2023, variable-rate segments, such as structured credit, benefited from the rise in interest rates while the other segments suffered from the underperformance of the price component of bonds. The table below illustrates that while no two years are alike - and the same holds true for performance contributors - this is advantageous for investors in segment-agnostic funds.

The second advantage is the construction of a portfolio of strong convictions that is also diversified. A credit index comprises a large number of issues (for example, a “high yield” credit index comprises around 300 issuers). Although credit markets are efficient too some extent they are less so than equity markets. It is therefore reasonable to assume one can identify 15 to 20 issuers whose fundamental risk is poorly assessed, and therefore represent an attractive investment opportunity. This logic can be applied within each credit segment. In terms of portfolio construction, using a broad universe (6 to 7 sub-segments as illustrated in the table below) enables the construction of a portfolio of 100 to 150 issuers on which the portfolio manager has been able to form a strong conviction and whose fundamental risk seems to be particularly poorly appreciated by the market.

Contributors to the performance of our credit fund (Carmignac Portfolio Credit)

«The daily ups and downs of interest rates, and therefore of bond asset prices, is a factor that bond investors will also have to take into account more closely in the future.»

Daily interest rate volatility is something that bond investors will also have to take more into account in the future. The MOVE index, the indicator of expected volatility for US Treasuries, currently anticipates daily movements of 8 basis points (bps), up or down, compared with an historical average of + or - 3 bps daily moves over the last twenty years. These changes in interest rates will naturally lead to wider variations in bond prices, which will have an impact on the risk/return potential of passive management, and having a view on the price of these assets will enable active investors to identify buying and selling opportunities.

1From mid-2010 to mid-2011. The Morningstar Category (EAA Fund EUR Flexible Bond) returned +4.4% and the market (Bloomberg Euro Aggregate Bond Index) posted -0.13%.

2During the period the average actively managed fund returned +2.39% (Morningstar Peer Group) compared to the euro-denominated Aggregate Global Index which posted negative returns of -0.33%.

3The Morningstar category posted -8.56% versus -17.17% for the Euro Aggregate index.

4 Bloomberg Euro Aggregate Bond Index, as of October 2023.

5 Carmignac Portfolio Global Bond.

6 Bloomberg Barclays Global Aggregate index.

Main risks of the funds

Carmignac Portfolio Global Bond A EUR Acc

Recommended minimum investment horizon

Lower risk Higher risk

CREDIT: Credit risk is the risk that the issuer may default.

INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates.

CURRENCY: Currency risk is linked to exposure to a currency other than the Fund’s valuation currency, either through direct investment or the use of forward financial instruments.

DISCRETIONARY MANAGEMENT: Anticipations of financial market changes made by the Management Company have a direct effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

Carmignac Portfolio Credit A EUR Acc

Recommended minimum investment horizon

Lower risk Higher risk

CREDIT: Credit risk is the risk that the issuer may default.

INTEREST RATE: Interest rate risk results in a decline in the net asset value in the event of changes in interest rates.

LIQUIDITY: Temporary market distortions may have an impact on the pricing conditions under which the Fund might be caused to liquidate, initiate or modify its positions

DISCRETIONARY MANAGEMENT: Anticipations of financial market changes made by the Management Company have a direct effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.